Don't be on

the road to nowhere

Our viewpoint

6 December 2021

Like the old Talking Heads song, without direction DC schemes risk being less effective.

Our latest DC survey highlights that overall, only around half of respondents have some kind of metrics or objectives in place for measuring the effectiveness of their DC scheme.

Currently have any agreed metrics for the management of the DC plan - By size of organisation

Error loading Partial View script (file: ~/Views/MacroPartials/Turtl.cshtml)Perhaps as expected, this increases to two-thirds for larger organisations, where they are likely to have greater resources at their disposal. This is good news for the DC savers in these schemes, providing the metrics are aligned to suitable objectives. The survey reports the main areas measured are participation rates and engagement levels.

Metrics used in the management of the DC plan - All respondents

Error loading Partial View script (file: ~/Views/MacroPartials/Turtl.cshtml)With the demise of ‘gold plated’ defined benefit pensions, the reality of retirement for many DC savers will be a gradual transition from working to not working, for example alongside reducing working hours. As DC pensions become increasingly significant to an employee’s ability to retire, for businesses (and for succession planning purposes) it will be vital to make sure DC schemes are as effective as they can be and deliver the best outcomes.

We are all aware that it is increasingly common for employers to outsource their pension arrangements, for example to a master trust or a group personal pension. Whilst this will be the right answer for many organisations, there is a danger that in doing this, employers believe they no longer need to get involved and that the provider and / or master trust trustees will make sure everything is covered. In fact, the survey shows that organisations with trust based schemes are more likely to have metrics in place than those with master trusts or group personal pensions.

Master trust trustees and Independent Governance Committees (IGCs are responsible for oversight of a provider’s group personal pensions) have huge diverse populations (in some instances millions) of active and deferred DC savers they are responsible for, across multiple employers. The effect of this is that whilst they must act in the best overall interest of their DC savers, because of the diversity of the populations and their needs, governance and activity can tend to be relatively generic in its nature.

We believe for this reason employers with these schemes should also put in place their own oversight arrangements. By putting in place an oversight group, it is possible to achieve a best of both worlds’ outcome. Core standards of governance and compliance are delivered by the master trust trustees / IGC, and this is supplemented by employer led oversight focused on the needs of its particular employees.

But what should this group do?

Often, we find employers have already put in place an oversight group, so clearly, they feel that there is something they need to do. After all, with auto-enrolment increasing take up and contributions, millions of pounds are flowing into DC schemes on behalf of employees and the amounts invested are set to multiply rapidly over the coming years.

But all too often we find that the group lacks focus and is not clear on what it is trying to achieve. A common scenario is that they will meet once or twice a year, review the provider’s “management report”, hear from them about new services, communication options and tools, but no firm focused activities are undertaken. Groups can often be distracted by well-meaning offers of new services or lots of data from their provider, rather than focusing on what’s important for them.

One of the major activities should be to hold the provider to account, for example to make sure they deliver what they promised when they were appointed. Also, it is not uncommon for things to change (just consider ESG recently), so monitoring if the provider is keeping up with best practice and ultimately if they are not, calling for a review of the provider.

We advise clients to have clear agreed objectives for these groups and it makes sense to align them to issues that will improve their employees’ retirement outcomes, as ultimately this is what the oversight group should be there to do. Normally we would have measures set around:

- Participation rates and contribution levels

- Investments and charges

- Administration delivery

- Engagement levels

- Accessing benefits – when and how

The measures and objectives need to be agreed by the oversight group, tailored to their scheme, reflecting what the employer wants to achieve and also the profile of the membership.

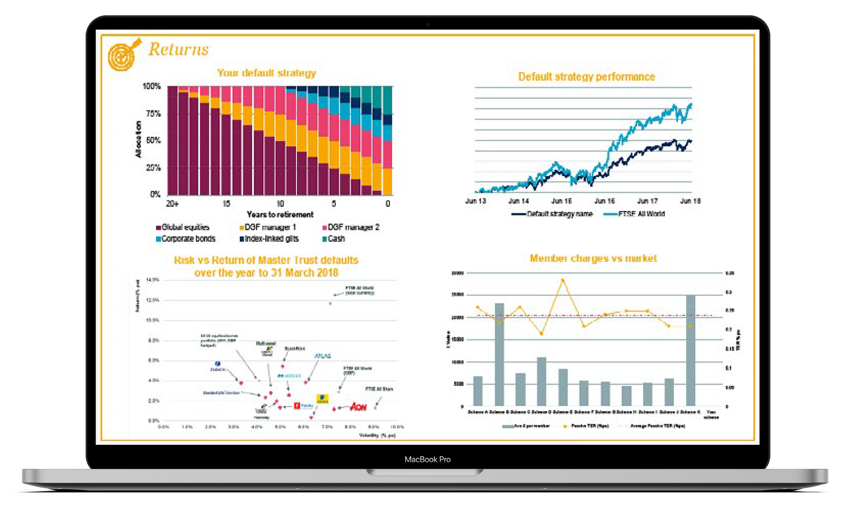

LCP produce a short DC Dashboard for clients we advise in this area which is designed to quickly and efficiently show progress against each objective and give a market context to each measure, ie how a scheme compares to others. Normally the oversight group have day jobs and are therefore time constrained when it comes to pensions, so reviewing a simple snapshot of scheme metrics is what they need. The oversight group will undertake prioritised activities (for example harnessing the master trust scheme resources) and the Dashboard will be updated to document progress against the objectives at least annually.

What next?

Make sure you have clear objectives set out for your DC scheme preferably aligned to improving DC saver outcomes and review your progress against these objectives regularly.

Rolling on the river

The right direction but still a way to go for DC schemes

Find out the results of our DC survey in our report which explores the implications of them for the outlook of DC pensions.

Read the report