PPO propensity:

what can we learn from the pensions industry?

Our viewpoint

18 February 2019

One of the continuing mysteries in the insurance world is why so few claimants take PPOs, which are designed to protect them from longevity risk and investment risk. The latest statistics show that only around 10% of potential claimants take a PPO (PPO Working Party - 2018).

A PPO is essentially identical to a pension, and so where better to learn about this mystery than from the pensions industry?

A recent paper “Survival pessimism and the demand for annuities” published by the Institute for Fiscal Studies looks at this from the opposite angle – why do so few retirees purchase annuities despite the longevity insurance they provide?

The paper starts off by explaining the “annuity puzzle”.

Annuities insure individuals against longevity risk by allowing them to exchange wealth for an income stream guaranteed until death. Theory predicts that under general conditions, risk-averse individuals will purchase a fairly-priced annuity…Few households, however, ever purchase an annuity.

It turns out that the key phrase here is “fairly-priced”, and, in particular, people’s perception of what constitutes fair.

More specifically, individuals have their own idea of how long they are likely to live. If this is shorter than the insurance company assumed when pricing the annuity, then the individual will not buy the annuity.

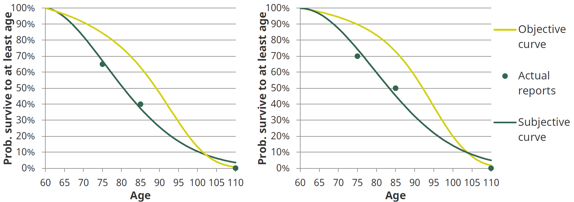

The paper builds a picture of subjective survival probabilities based on a large survey of the English population aged 50 and above. The conclusion is that individuals in their 50s, 60s and 70s significantly under-estimate their life expectancy. Older individuals actually over-estimate, but they are not the core targets for annuity purchase.

If someone under-estimates their own life expectancy, this means that they will perceive an annuity as poor value for money, even if it is fairly-priced.

So, what does this mean for PPOs?

Essentially, the individual is faced with the similar choice to the annuity purchaser – should they take an immediate, large, lump sum; or should they take a PPO, with income guaranteed for life?

There are secondary considerations, just as there are when buying an annuity. For example, distrust of the insurance company that they will now be reliant on for life; the increased utility of a large lump sum to facilitate immediate purchases; misunderstanding the effect of discounting (whether it is at the current statutory level of -0.75% pa, or the higher rate at which most settlements are effectively made).

However, if we focus on the longevity issue, we are faced with the same question as discussed in the paper. Based on the conclusions from that paper, if so few individuals take a PPO, it should be that they are under-estimating their life expectancy, just like retirees are.

With PPOs, which are often for individuals with severely impaired life expectancy, assessing longevity is even more difficult. Typically, within any negotiations, each side will have their own expert, and these experts can differ greatly in their assessment of life expectancy. It is not uncommon for the injured party’s expert to advise a figure, say, 10 years higher than the insurance company. The lump sum will be based on a compromise somewhere in between.

What this means is that the lump sum is calculated based on a life expectancy that is less than that advocated by the injured party’s expert. This should make the lump sum appear poor value compared to the annuity, making the PPO more attractive.

This is the opposite of the annuity purchase case, where the conclusion from the paper was that people don’t buy annuities because they believe they won’t live as long as assumed in the annuity price, making them appear poor value.

So, having learned our lessons from the pensions industry we are left with a paradox as to why so few claimants opt for PPOs when the economic theory says that they should.

One possible explanation is that they don’t really believe what their experts are telling them about their life expectancy. I look forward to hearing your solutions to this paradox.

Solvency II reporting across the UK and Ireland

Market survey

Our third annual review of Solvency II reporting by 100 of the top non-life insurers in the UK and Ireland.

Access the findings