Getting better value from

Actuarial Function opinions – Part 2

Our viewpoint

28 July 2021

“Actuaries are seen as the team that turns up 6 months late and says what we could have done better.”

This comment from an insurance NED reflects the views of a number of board members that we have spoken to recently about the actuarial function’s work and in particular the formal opinions.

My previous blog set out three principles that should underlie every stage of the actuarial function opinions:

- Target value-add, not (just) compliance

- Actuarial function activities should occur before decisions are made

- Achieving best practice may be an iterative process

There I set out how to apply the first principle to technical provisions. In this blog I discuss how you can apply the second principle to the underwriting opinion.

Actuarial function activities should occur before decisions are made

Some firms get a lot of value from the underwriting opinion; however, in our experience, many others do not. Often this is because the actuary’s opinion, however thoughtful, arrived too late to make a difference. We have produced a guide on the underwriting opinion process showing examples of best practice, good practice and some behaviours to avoid. This blog covers two aspects of the underwriting opinion: the business plan, and rate adequacy.

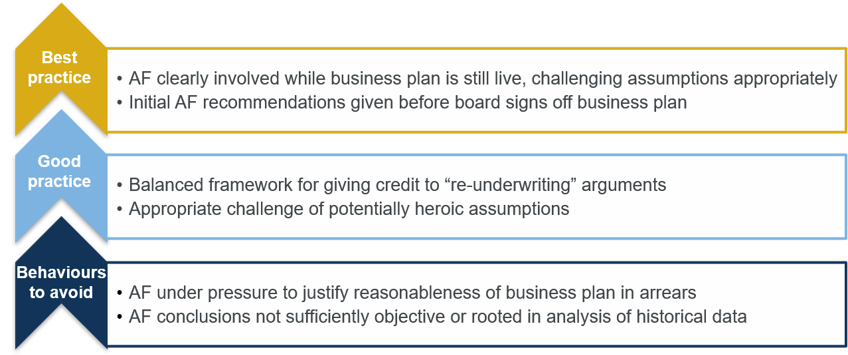

Business plan

Every firm is different, and so every business plan is different. However, every company has a regular process of planning involving senior management, finance and the board. In most cases this process is time pressured and it can often be difficult for the actuarial function to make a meaningful impact while the business plan is still live. If not, then they run the risk of having to retrospectively justify aspects of the plan because it can’t be changed, which doesn’t add any value to the business.

We have found that some of the best challenges are the simplest, for example “What is our justification for assuming that can we increase business volumes at the same time as increasing premium rates?”

Another simple method of challenge is to compare the business plan loss ratios to the trend of historical loss ratios and to highlight any obvious difficulties, eg assuming that the business will reverse a historical trend of worsening loss ratios simply by “re-underwriting” the book.

The skill of the actuary is to present the facts to the board in terms that it understands. For example, the actuary can show how much advance credit is being taken for underwriting changes and give the business the information it needs to decide whether this is a reasonable assumption or not.

Before the board signs off the business plan, it should have (at the very least) the actuary’s initial observations and challenge, even if this is not yet set down in a formal opinion.

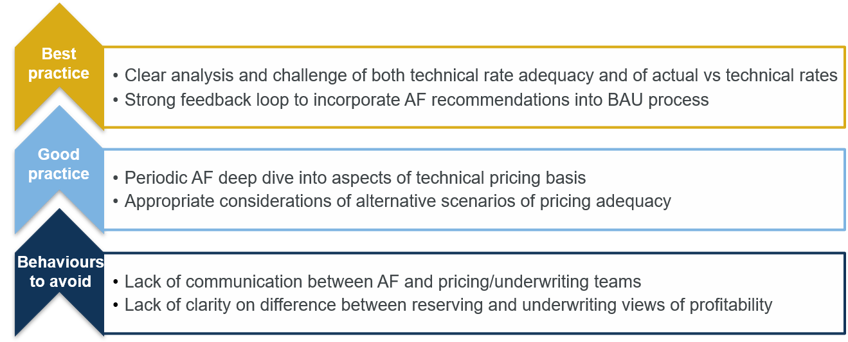

Rate adequacy

The actuary’s views on rate adequacy and the business plan are often closely aligned. The key for the actuarial function is to kick the tyres of the pricing approach, without getting too much into the detail of the rates themselves.

Here, analysis of the variation of actual rates from technical rates can be really useful. There should be clear reasons as to why historical deviations are at the level observed, and the board should understand the implications for future profitability.

Differences in terms and conditions are often rolled up into the analysis of rate changes. It can be difficult to measure the effect of T&Cs objectively and it is important that the actuary finds objective measures to assess against and provide appropriate challenge. One method that can work well is to “back-solve” the effective allowance for change in T&Cs in the rate change and play this back to the underwriter to confirm it is reasonable.

The underwriting team will have used certain assumptions to inform the premium rates. There may well also be differing views on the profitability of the business between the reserving and underwriting teams. This is perfectly proper, and the actuary can help the board understand the reasons for differences by illustrating plausible alternative assumptions both adverse and favourable, and by showing the effect on profitability of using the reserving actuary’s (potentially less optimistic) assumptions.

Throughout this process the actuary should not only be asking the difficult questions but also encouraging the underwriting and finance teams to build these questions into their own process, so that the first cut of the business plan already addresses the likely avenues of actuarial challenge. Getting involved while the business is still at the planning stage creates a strong feedback loop that increases the chance that recommendations are converted into business as usual.

Next time I will take a further look at the underwriting opinion, focusing on anti-selection and emerging risks.

The Virtuous Cycle

Thought Leadership Report

A comprehensive guide on how insurance boards and actuaries can work together more effectively. This is based on in-depth interviews with 25 leading UK general insurers across the market to understand how they make key business decisions based on actuarial advice.

Explore our findings