Credit investing –

to match or not to match. Is that the question?

Our viewpoint

19 October 2020

Andy Linz analyses the benefits of combining shorter-dated credit alongside long-term cashflow matching.

At a glance:

- As pension plans mature their investments need to generate cash to pay benefits as they fall due. One approach that is particularly popular is cash flow driven “matching” – matching cash flows from bond assets to expected liabilities

- Our analysis shows that holding a combination of shorter and longer dated credits can lead to better outcomes than building a portfolio of only long-dated “cash flow matching” credits to pay long-term liabilities.

- This is because shorter dated bonds provide some protection in tough credit environments, provide re-investment opportunities and reduce default and downgrade risk exposures.

“Matching” has an inherent attraction for investors looking to increase the certainty of their returns. If a bond is held to maturity and the expected payments are paid in practice then the investor knows exactly what return they will get (we’ll set aside uncertainty about how much we might need to pay for now).

But is maximising matching the best way to go? Let’s consider the risks. Three of the key risks investors take when investing in credit are:

- Default risk – the risk that the bond issuer doesn’t make the payments it has promised.

- Downgrade risk – the risk that the creditworthiness of the bond issuer worsens and credit ratings and bond prices fall.

- Reinvestment risk – the risk that the return available on bonds we want to buy in the future is lower than what we expect.

If we are aiming to pay a future cash flow, buying and holding a bond to maturity where the pay-out date lines up with our liability cash flow (ie matching) can eliminate our exposure to downgrade risk and reinvestment risk. We don’t mind what the market prices of our bonds or other bonds available in the market are, as long as we receive the payments we have been promised. This means our only risk exposure is to default risk – which we may expect to be reasonably low for high quality bonds.

By contrast, if we invest in a portfolio where we are buying credits in a fairly short turnaround and don’t hold on to them for an extended period we can reduce our default risk but we may still find ourselves exposed to downgrade risk and so take much more reinvestment risk.

What does it look like in practice?

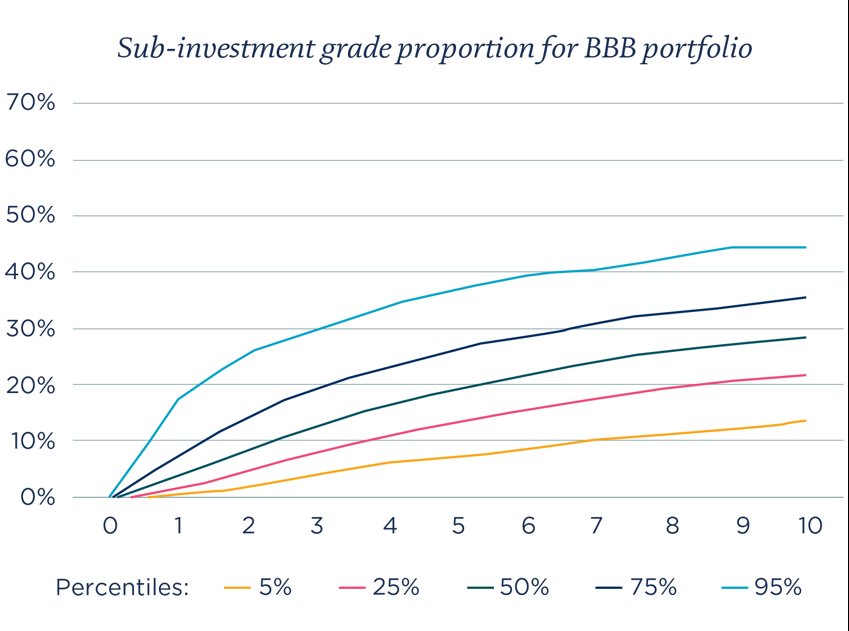

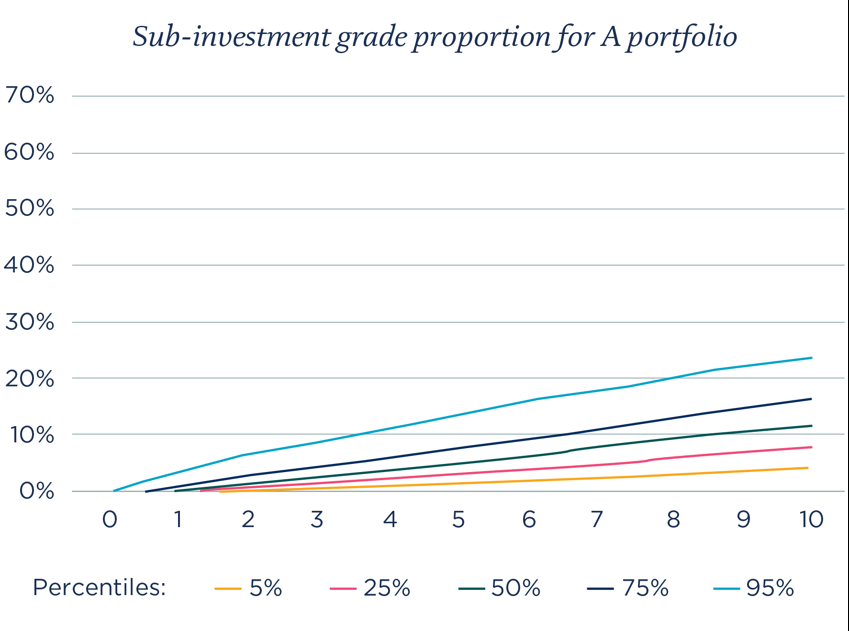

This all feels very theoretical, so let’s try and make it a little more real world: How might a matching portfolio where bonds are bought and held to maturity work in practice? The charts below show the percentiles of how much sub-investment grade exposure we might expect a buy and hold portfolio starting with a given credit rating to have after 10 years.

Source: LCP analysis

This means that for a buy and hold portfolio of starting credit quality BBB we might expect there to be a 50-50 chance of just under a third of the portfolio being sub-investment grade ie “junk” by the end of year 10. For a portfolio of single A quality this might be around 10% of the portfolio.

In our view, most pension scheme trustees would avoid constructing a matching portfolio with these junk grade bonds and would prevent a manager from having such a high proportion of lower quality credit assets in a low risk matching portfolio. This is why we see many mandates of this type setting rules limiting the proportion of sub-investment grade in their portfolios – some of this exposure would likely be sold in a real portfolio.

Rather than pure buy & hold strategies we might instead look at matching strategies which sell bonds which fall below investment grade quality. This means we expect to have some downgrade risk in our matching portfolio as well.

Mix and match?

A matching portfolio like this could experience difficulties if there are high levels of defaults and downgrades. Usually this would be in a stressed environment and would be accompanied by widening credit spreads. The question is, can we improve on a pure matching approach by including some assets we expect to do well when spreads widen?

Investing in a rolling portfolio of short-dated credit gives us this possibility. Impacts from wider spreads on the value of the short-dated bonds we already hold are likely to be fairly small, but when we reinvest it will be at higher credit spreads. Reinvestment risk can become reinvestment opportunity under the right conditions.

The opposite is also true. When spreads are compressed, we expect to have a lower number of defaults and downgrades, so our matching portfolio performs better than expected when the re-investment rates of the rolling strategy are low.

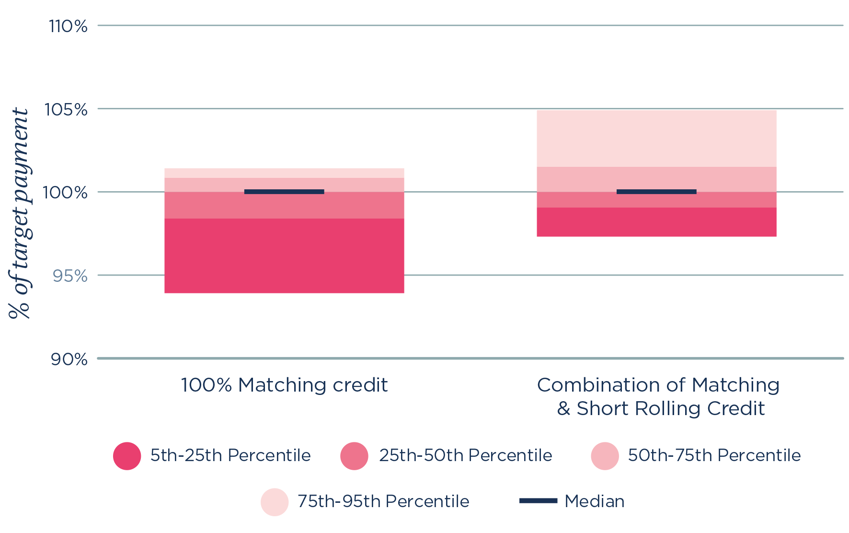

This is promising – we have an investment approach that offsets some of the risks of a pure matching strategy but still offers a similar level of expected return. We performed detailed analysis on combining these strategies. The below shows some of the results – looking at the spread of outcomes for paying a fixed cash flow in 10 years’ time.

Strategy outcomes for 10 Year target strategy

The results indicate that holding a short-dated credit portfolio with a rolling reinvestment programme alongside a longer-dated matching credit portfolio can improve outcomes. In terms of both downside protection and potential upside the more diversified approach appears more efficient.

Strength in diversity

Should we be surprised? It’s not for nothing that Harry Markowitz, the architect of modern portfolio theory, described diversification as the only free lunch in investing. It’s not a lesson to forget as pension schemes look to plan their de-risking journeys.

In my view and as our analysis supports, it’s more efficient for a pension scheme to hold a diversified portfolio of assets, including both shorter and longer-dated credits, rather than a portfolio concentrated in long-dated “cash flow matching” credits. Focussing on the return needed and how it can be generated as efficiently as possible with sensible liquidity management and use of income is a key part of our investment philosophy. See more on this from my colleagues Gavin and Dan here.

Shifting sands 2020 - for corporate sponsors

Thought leadership report

Exploring four key areas - managing corporate pensions in the current environment; how sponsors can take the initiative on investment; hot topics; and preparing for the year-end.

Explore our findings