Questions

for your covenant adviser

Our viewpoint

23 August 2019

How well have you TESTED the impact of your covenant on your investment strategy?

“It’s good to talk” was the strapline of a well-known UK TV advert in the 1990s. But it certainly applies in 2019 when you are working alongside other advisers to the trustees of a DB scheme. Even better when you can ask each other the right questions to get at the key issues and risks for trustees to focus on. This ultimately leads to better decisions, informed by a holistic view of the scheme, and better outcomes for members.

We set out our blueprint for joined-up journey planning and risk management in our recent thought piece Chart your own course. But trustees often tell us that it can be hard to join up the advice they receive from these different advisers: they talk, but often not in quite the same language. This can be particularly true in understanding how your covenant drives how you approach your investment strategy - for example the level of risks you can afford to run and what covenant support might be available if investment performance is poor.

As an independent consultant with actuarial, investment and covenant skillsets working together under one roof for our clients we see practical examples of how advice can be pulled together effectively every day.

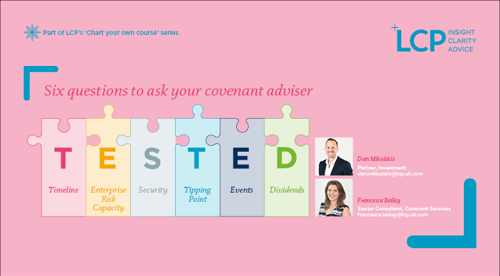

Here are six questions you or your investment consultant could ask your covenant adviser to get you thinking about how covenant integrates with investment strategy.

- Timeline: are there specific milestone timepoints in the sponsor's business (eg rolling over of key customer or supplier contracts, patent expiry, debt profile, customer lifecycle)? - these can affect the decision around when to aim for full funding.

- Enterprise risk capacity: key affordability ratios can shed light on what the covenant can reasonably support (eg free cashflow divided by pension deficit plus Value-at-Risk.1) Is the coverage high or low compared to the overall universe and what you would expect given the covenant grading?

- Security: are there viable options for contingent security that might be negotiable with the sponsor (eg properties or asset-based funding arrangements)? If these are available, it could significantly change the ability to underwrite risk in the investment strategy.

- Tipping point: is there a tipping point that could come into play with respect to debt rating or covenant grading and what are the key variables influencing that? The trustees will want to form a contingency plan with respect to investment strategy, perhaps reducing risk or changing the endgame target.

- Events: what are the key events to watch out for which the trustees should put contingency plans in place (eg takeover, debt-funded M&A, regulatory fine, loss of key customers, business unit spinoff). The trustees have levers they can pull on the investment strategy: more or less return, longer timeframe, different objective, change of strategy. But having a contingency plan in advance is key.

- Dividends / leakage: what is the level of dividends vs deficit contributions, and what other forms of covenant leakage could be possible over the period of the journey plan to full funding? Again, forewarned is forearmed and the trustees can form a fall-back plan on the investment side which might involve a change of endgame target, risk budget and strategy.

But, don’t forget that the answers to these questions can change over time.

So if you are aiming for a governance and monitoring framework that is best in class and robust over time:

- Make sure you are proportionately monitoring your sponsor’s covenant strength, using the right monitoring metrics and triggers for call-to-action.

- Make sure any changes are efficiently communicated across all your advisers so that actions can be taken if needed.

- Set contingency plans in advance, so you know what you can control, and how to react.

1Value-at-risk or “VaR” is a measure of how much bigger the deficit could become over a defined period of time. For example, if the one year 95% VaR was £100m, that means that there is a 5% chance that the deficit could increase by £100m or more in the next 12 months.